The Good Relationship

A blog that knows money is never just the numbers

Click a category to dive deep:

Relationship with Money

Sustainable Income

Accessible Saving

Why We Love Our One Pager

Why We Don’t Manage Assets

Content Spending

Patient

Investing

Why We Don’t Predict

Why We Prefer a Flat Cost

243 | When We Need it Most

The quality of our saving all comes down to access.

Because the same number means wildly different things to different people.

And wildly different things to the same person in a different season.

But the ever-present question with saving is…

Can I tap into what I’ve set aside when I need it most?

Sometimes we pick when we “need it most” and sometimes we’re volun-told.

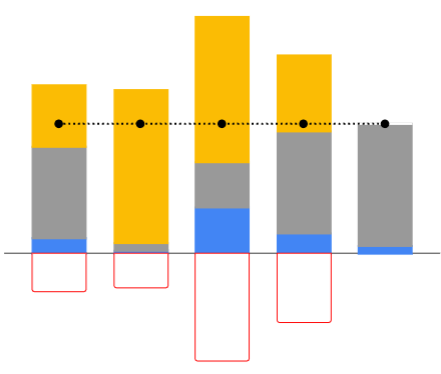

So here we are, five equally “wealthy” people…

The numbers say they’re the same net worth - the black dots - or the sum of the blue, gray, and yellow less the red.

But which would you pick to be yours?

Does it matter if you love your job?

Or if you hate it?

What if a big spending decision is looming?

Or if one has finally moved behind you?

What if you want to be more generous?

Or if you have a habit of creative generosity?

What if you’re in a season that allows you to save?

Or a season that is forcing you to dip into savings?

We could keep asking questions, but they’ll keep highlighting the fact that saving is more art than science.

227 | Smoke Signals

Where there is smoke, there is fire.

And two smoke signals billow up at every level of financial wealth.

Cash on hand, or the Blue bar as the locals know it, is the first one.

No matter the net worth, the most content folks are those with enough cash to ignore their next paycheck and the ups and downs of their investments.

But the lower the cash goes, the hotter the embers burn.

Savings rate, or the Green bar, is the second one.

If you aren't saving,...

- You're living beyond your means,

- You're surprised by some unexpected things, or

- You're spending now to see some benefit later

It's OK to have seasons without saving, particularly if you started it with enough Blue, but if you keep poking the embers you eventually fan the flame.

If you’re getting that “things-feel-a-little-tight” vibe, look for the smoke and then work to put out the fire.

Extra Perspectives

You Aren’t Too Big To Fail (And That’s Okay) by Jared Korver

221 | You Don't Need a Roth to Retire

This might be hard to believe (because it's where most financial advice begins and ends), but you don't need a Roth IRA to retire.

And you don't need a 401(k) either.

Just ask the wealthiest people around where most of their wealth sits - it's neither of those spots.

It's easy for the type of account to distract us from what is happening with our finances.

The income that gets saved is the gas being pumped into the car.

The account where it is saved is unleaded 87 versus unleaded 89 - a basic shuffling of costs between now and later.

An extra quarter tank of gas is how you ensure you reach the destination - not a fuel upgrade.

209 | Negative Numbers

A credit card balance is a checking account with a negative balance.

If you envision it any other way, you’re confused about how they work.

Harsh? Blunt? Too direct?

That's the only option when something can escalate from fun and innocent to dangerous and overwhelming so quickly.

Travel perks don’t make it positive.

Sign up bonuses don’t either.

In fact, nothing turns it positive.

You can only get it back to zero with a transfer from a positive checking account.

208 | Shocks on a Car

Cash in the bank is like shocks on a car.

If you’re feeling every single bump – or stressed about every purchase – then adding some shocks will help.

The feeling of the bumps doesn’t mean the engine is bad.

Or we’re headed the wrong direction.

Or we need a different car.

We just need some more shocks.

156 | Seasons of Transition

In a season of transition*, two things matter…

How much cash do you have on hand?

How much is that amount changing each month?

If we don’t begin with enough cash on hand, it’s going to be a stressful, hopeless transition.

If cash is decreasing, then we need more income or less spending – there are no other hacks.

If cash is staying flat, then we’re doing something right.

If cash is going up, then we can start talking about everything else.

*Career change, more income to less income, no dependents to some dependents, old home to new home, etc.

74 | Cash Gets a Bad Rap

If there was a contest for biggest buzz-kill in finances - talking about "cash on hand" might take the cake.

Usually, it gets paid a measly interest rate.

Usually, it just sits there and "doesn’t do anything".

Sometimes there is a temptation to spend it all or invest it all - neither of which is a very good idea.

To top it off, cash in the bank is often called an "emergency fund". Talk about negative self talk!

It's tough because the measurable things aren't that impressive.

All the cool parts about cash are the things you can't measure - the ways it allows you to organize your life without thinking about the dollars needed.

Cash allows you to say "yes" to the opportunity of a lifetime or the year or the month without "crunching the numbers".

Cash allows you to change jobs or careers.

Cash allows you to take time off between jobs.

Cash allows you to ignore the due date on your paycheck because you're not waiting for those dollars.

Cash allows you to ignore the due date on your credit card bill because it's on auto-pay and you know the funds will be there.

Cash allows you to leave investments alone when they're down 20% in a 12-month period.

Most people I know want opportunities, options, and flexibility, which is exactly what cash offers, but we just don't think of it that way.

Google says three to six months of expenses is an appropriate amount of cash to have on hand, but if collectively we all feel limited or constrained by our money, doesn’t that make you think the standard rules of thumb might need a little work?

If you want more opportunities, options, and flexibility, try holding a little extra cash and see what happens.

Additional Reading

How I Think About Cash by Morgan Housel

How Your Bank Balance Buys Happiness: The Importance of “Cash on Hand” to Life Satisfaction by Peter M. Ruberton, Joe Gladstone, and Sonja Lyubomirsky

54 | Seesaws and "Enough"

Our kids love a seesaw - the constant ups and downs seem like Roller Coaster 101 for those under the age of 6.

The "pivot point" in the middle of the seesaw on which the entire board rests is the fulcrum.

The closer you get to the fulcrum, the harder it is to lift the other side.

The further away from the fulcrum, the easier it is to lift the other side.

A 4-year-old way out on one end can lift someone many times his or her size if that person is close to the fulcrum.

And vice versa, no amount of force applied near the fulcrum is going to lift the 4-year-old into the air.

Of course, I see a connection to finances. How can I not?

Income that is not accompanied by an ability to spend less than 100% of it is like applying force at the fulcrum of the seesaw while "enough" is sitting way out on the end.

Even for folks, especially for folks who have the highest levels of income*, the reality holds true.

The force matters, but only if the fulcrum is in a place to leverage it.

If the fulcrum is in the wrong spot, no amount of force is bringing the other end off the ground.

It's not about applying force, or generating ever-increasing amounts of income, until you retire, burn-out, or quit. It's about slowly adjusting the position of the fulcrum to see "enough" begin to come off the ground.

Of course, no seesaw is ever perfectly still, but once we know the mechanics, it's easier to predict which way we're headed.

When it comes down to it, I think deep down everyone just wants to have "enough", but it's all too easy to forget the role of force and the role of the fulcrum.

*I caught myself typing "fortunate enough, lucky enough, talented enough to have high levels of income" and realized my own biased towards "more" being the default best case scenario.

43 | Why So Many Bank Accounts?

Any time I see a bunch of bank accounts within a single household...

I cringe a little bit.

Yes, I understand the mindset of segregating money for a specific goal from everything else.

I see how having separate accounts in a relationship could allow spending to happen seamlessly without a value judgment being placed on each purchase.

I also know that a business owner needs to keep the business finances separate from personal finances.

Certainly there are other advantages that I am not listing.

I can buy into each of these advantages if they are done with clear intention, but it also doesn't have to be this hard.

The number of disadvantages to allowing your list of accounts to grow without pruning seem infinite and hard to measure from a psychological perspective.

When everything comes into one place, and everything goes out of one place, it makes it a lot easier to do something that is important in finances...

Keep track of how much is coming in and how much is going out.

This sounds so simple, but it's so easy to overlook.

When funds are spread across a bunch of different accounts…

It's a lot harder to keep track of what is real income and what's a transfer between your own accounts.

It's close to impossible for the average person to keep tabs on where dollars are being spent.

It's a lot easier for things to run on autopilot for many months or years longer than they were intended to run in the first place.

It's a lot easier to panic when an account balance gets low even though your collective account balances are more than enough.

When it comes to the number of accounts, "Less is more!".

42 | Running on Empty

This past weekend, my dad and I were riding down to Pinehurst to meet up with my brother for a weekend of golf, college basketball, and quality time.

Pinehurst has been a special place to all three of us for many years - U.S Opens, golf weekends, and visits to my grandparent’s-in-law house.

Over the past 15 years, I'd bet that I have driven the route from Winston-Salem to Pinehurst somewhere between 25 and 30 times.

I know the route well - the food options, the golf courses we pass along the way, the exits with tons of options, and the exits without much of anything but an on/off ramp.

About seven miles away from the traditional turn off, we passed an exit with our last gas station option. As we drove under the overpass - the exit officially behind us - Dad said, "I think we should be able to make it to the next exit before we have to fill up."

At this point, the warning indicator read, "1 Mile to Empty".

For a few minutes we chuckled as we discussed the decision - how long has the light been on? Does the light coordinate with the mileage counter? Does "1 mile" mean 1 mile or does it mean 35 miles?

Based on prior experience, we sensed that we had some leeway, but the exact amount of leeway was unknown and the previously casual discussion quickly pivoted to how far we were from the next gas option.

After a few minutes, we began approaching the normal exit and saw big, orange barricades across the entire ramp - "EXIT CLOSED".

The innocent chuckles and "what ifs" of a few miles back pivoted further into somewhat nervous laughs and a quick glance at Google Maps to assess the reality of the situation.

At this point, we were winging it on what seemed like a gallon at the most and fumes at the worst.

The innocent decision to pass on an easy gas stop seemed like no big deal until the next option, which had been available every time before, was not available at the precise moment we needed it.

The reality is that cash in a savings account is a lot like gas in your car.

With a full tank of gas, you can access exponentially more destinations than you can even with a half tank. The next fill up is way down the list of things you need to be concerned about and you have the freedom to dream and adventure without being too concerned with immediate logistics.

When you're driving on fumes or even a gallon, you are constantly thinking about when, where, and maybe even if you will be able to fill up again. You're completely susceptible to any uncertainty that is thrown your way. Even routine trips begin to feel reckless because there's a chance it won't go as smoothly as it always has.

With the gas tank, it is easy to see the cause and effect. With money, that relationship is not as obvious.

Ample gas in the tank, or cash in the bank, can feel like such basic advice that it's easy to overlook under the presumption that you'll always have the ability to fill it back up.

No matter the car, if you run out of gas, you're stuck.

No matter the level of wealth, if you run out of cash, you're stuck.

Fortunately, the next exit was only a couple of miles down the road. It didn't have a gas station, but we were able to navigate back to the closed exit in a roundabout kind of way to fill up the tank and grab lunch.

For us, the worst outcome would have been waiting on the side of the road for AAA and possibly missing a tee time for the afternoon. A bummer, but not a life changer.

With finances, the stakes can escalate much more quickly. The AAA equivalent when you run out of cash in a savings account is carrying a balance on a credit card out of desperation, selling investments at an inopportune time, or being forced to say "no" to something that might have been an automatic "yes" with more cash on hand.

Don't run your household on fumes!

Additional Reading

How your bank balance buys happiness: The importance of "cash on hand" to life satisfaction by Peter M. Ruberton, Joe Gladstone and Sonja Lyubomirsky

"Could liquid wealth, or "cash on hand" - the balance of one's checking and savings accounts - be a better predictor of life satisfaction than income?"

How I Think About Cash by Morgan Housel

"When chaos hits, nobody has enough cash."

40 | Why Do We Save?: The Most Powerful Reason

We save to keep our expectations in check.

A dollar that is not saved is spent - creating expectations.

A dollar that is not spent is saved - creating options.

The challenge is that every dollar gets assigned to either expectations or options - you can't pick "both" and you can't pick "neither".

This fact alone makes it the most complex relationship in our personal finances and the thing that most financial well being hinges upon.

A weekly coffee, a monthly streaming subscription, an annual trip, a specific school, a specific style of decorating a home - each has a different purpose, magnitude, and frequency, but every single one creates some degree of expectation.

When expectations grow out of control, eventually there is a day of reckoning and reality forces us to push the reset button.

When options grow out of control, there are a number of downsides too, but they're a conversation for another day.

The purpose here is not to determine an objectively correct level of spending/saving or make a value judgment on different types of spending.

Both are impossible tasks.

The purpose is to acknowledge the power of saving and its role in a world where expectations are easier than ever to create and as painful to change as they have always been.

39 | Why Do We Save?: The Underrated Reason

We save in order to keep flexibility in our finances.

A habit of saving - income (purple) consistently exceeding spending (red) - is the equivalent of playing a card game with wild cards.

The flexibility and combinations that come from having wild cards in your hand completely changes every hand, every decision, and eventually the entire game.

If you have an established habit of saving then you can...

Take a pay cut to make a career change or shift to part time without changing your underlying lifestyle.

Say "yes" to a once in a lifetime opportunity without crunching the numbers or wondering if you're being reckless.

Spontaneously give money to an organization or person that means something to you because you want to or because they have a specific need.

Temporarily re-direct funds that have historically landed in a bank or investment account and for a season cover college tuition or a car purchase or a trip.

The flexibility afforded by saving can be hard to wrap your mind around, because we think of "saving", or "not spending", as constraining.

It's too easy to think that "spend whatever you want" is flexibility.

In actuality, "spend when you want" is a truer form of flexibility that comes only from a habit of saving.

Additional Reading

Overstuffed by Seth Godin

38 | Why Do We Save?: The Obvious Reason

We save to set aside money that we can spend later.

OK...?

Tell me more please...

Not saving is like...

Routinely running your gas tank to empty. You're always looking for the next gas station, you're limited in how far you can travel, and you're always susceptible to a tiny change in plans or expectations leaving you stranded on the side of the road.

Buying food for your next meal only. There's no slack in the system in case you’re unable to go to the store tomorrow, someone else decides to join you unexpectedly, or you find out the food has gone bad.

Operating with only the roll of toilet paper that is on the holder. Once you get to the second half of the roll, you're going to be pretty aggressive with conservation and pretty selective with who you'll call if you happen to run out.

We have no problem operating with a little more gas or food or toilet paper than we need for the next moment. We're also pretty adept at not hoarding any of them.

In reality, money doesn't need to be any different, but for some reason it feels much more complicated.

With money, it's easy to do the equivalent of always operating on E or towing a tank truck of gas behind you so you never run out. Finding the right middle ground is so much harder.

Inevitably, every dollar spent over a lifetime is not perfectly timed with an offsetting dollar of income. This is the essence of why we need to save something.

What's challenging is that if this is the only reason for saving, eventually we're going to get burned out, forget why we're saving, or struggle to determine how much is enough.

25 | Homebuying Series: Wealth Is What You Don’t See

An excerpt from The Psychology of Money by Morgan Housel...

We should be careful to define the difference between wealthy and rich. It is more than semantics. Not knowing the difference is a source of countless poor money decisions.

Rich is a current income. Someone driving a $100,000 car is almost certainly rich, because even if they purchased the car with debt you need a certain level of income to afford the monthly payment. Same with those who live in big homes. It’s not hard to spot rich people. They often go out of their way to make themselves known.

But wealth is hidden. It’s income not spent. Wealth is an option not yet taken to buy something later. Its value lies in offering you options, flexibility, and growth to one day purchase more stuff than you could right now.

Diet and exercise offer a useful analogy. Losing weight is notoriously hard, even among those putting in the work of vigorous exercise. In his book The Body, Bill Bryson explains why:

"One study in America found that people overestimate the number of calories they burned in a workout by a factor of four. They also then consumed, on average, about twice as many calories as they had just burned off … the fact is, you can quickly undo a lot of exercise by eating a lot of food, and most of us do."

Exercise is like being rich. You think, “I did the work and I now deserve to treat myself to a big meal.” Wealth is turning down that treat meal and actually burning net calories. It’s hard, and requires self-control. But it creates a gap between what you could do and what you choose to do that accrues to you over time.

The problem for many of us is that it is easy to find rich role models. It’s harder to find wealthy ones because by definition their success is more hidden.

There are, of course, wealthy people who also spend a lot of money on stuff. But even in those cases what we see is their richness, not their wealth. We see the cars they chose to buy and perhaps the school they choose to send their kids to. We don’t see the savings, retirement accounts, or investment portfolios. We see the homes they bought, not the homes they could have bought had they stretched themselves thin.

The danger here is that I think most people, deep down, want to be wealthy. They want freedom and flexibility, which is what financial assets not yet spent can give you. But it is so ingrained in us that to have money is to spend money that we don’t get to see the restraint it takes to actually be wealthy. And since we can’t see it, it’s hard to learn about it.

People are good at learning by imitation. But the hidden nature of wealth makes it hard to imitate others and learn from their ways.

The world is filled with people who look modest but are actually wealthy and people who look rich who live at the razor’s edge of insolvency. Keep this in mind when quickly judging others’ success and setting your own goals.

11 | From Linchpin to Bottleneck

In a recent conversation with a friend, we discussed the strain on cash flow that often comes in the season of life with young children.

The strain can come from increased living expenses, reduced household income, or some combination of both.

For this particular friend, increased living expenses had impacted their particular situation and had led to a conversation around reducing their ongoing 401k contribution from 15% of their salary to 13% to provide a little cash flow relief.

The 15% rate was sound advice the friend had received right out of college and had lived into for nearly 10 years. Job well done!

In this current season, the savings rate had become an anchor that felt arbitrary, a little out of touch, but also untouchable.

Was a change "allowed"? Would a change knock them off track for saving for the future? Was a change the biggest "mistake" they could make?

A tactic that had once been the linchpin of financial freedom had slowly morphed into a constricting bottleneck in a different season.

I think behind these feelings sits the implied assumption that "more" saving is always better. The challenge is that sometimes "more" isn't possible and life circumstances demand something else.

Some seasons require "more" of other things - more time at home, more spending on things that are important, or more flexibility in where your savings land.

Your financial well being is not tied to the precise percentage that is saved into your retirement account for 30 consecutive years.

Your financial well being is more closely tied to your ability to slowly build resilience instead of grasping for certainty.