The Good Relationship

A blog that knows money is never just the numbers

Click a category to dive deep:

Relationship with Money

Sustainable Income

Accessible Saving

Why We Love Our One Pager

Why We Don’t Manage Assets

Content Spending

Patient

Investing

Why We Don’t Predict

Why We Prefer a Flat Cost

252 | Stay Squishy

The secret skill of spending is keeping it squishy.

Around here, spending is the red bar, and the size of that bar is only a sliver of the story.

The real story is its squishiness – how easily it expands and contracts and how easily it moves across time.

Squishy spending isn’t tied to the next paycheck, and it doesn’t require investments to hit another all-time high tomorrow – those are hallmarks of calcified spending.

Instead, it holds the tension of two opposing truths – 1) life costs money, and 2) every dollar spent builds an expectation of the future.

The trick isn’t avoiding spending but retaining the ability to pause it for a season or push it to another one.

A good litmus test for squishiness…

Am I committing myself (by obligation or preference!) to spend dollars this same way next year? In 5 years? In 10 years?

Honest “no’s” are a sign you're keeping it squishy, and often, a permission slip to say “yes” today.

If your goal is a feeling of freedom, stay squishy.

251 | The Good Relationship

Money, no matter the number of 0’s, will always be a relationship to refine.

Because there is no finish line or final destination - only habits and values to clarify over time.

The biggest risk - by far - is losing track of the story that our money is telling.

Which happens when we…

Get lost in the weeds.

Put our head in the sand.

Measure success only in dollars.

Expect perfection.

Keep secrets.

All of these, a natural, but broken way to relate to scarce resources and an unknown future.

But the good relationship extinguishes a scarcity mindset with healthy flows more than nest eggs.

And healthy flows look like…

Income that leverages natural gifts and skill sets. Allows for rest, breaks, and even leisure. Cares about endurance more than maximization. Draws us nearer to the people around us. Knows that every dollar before we break-even is priceless, and every dollar after break-even is not. Grows more pleasurable to earn over time.

Spending that slowly becomes a clearer reflection of who we are. Acknowledges that every dollar spent builds an expectation of the future. Adjusts in the face of uncertainty and disappointment. Respects the sneakiness of envy. Knows that generosity increases contentment, while debt does the opposite. Measures the quality of spending by its return, more than its cost.

Saving that understands its most important purpose is to govern expectations. Relieves the pressure of perfectly timed income and expenses. Knows that the landing spot is more art than science. Appreciates that cash on hand provides flexibility today and endurance tomorrow. Recognizes that saving too much is as harmful as not saving enough - it’s just harder to spot. Realizes that “saving”, or spending less than you make, is the definition of financial savvy.

Investing that is patient because it is informed (at least slightly) and committed (fully). Knows the two guarantees 1) someone will always outperform you, and 2) holding during scary times is the only way to succeed. Being an owner offers the most potential reward. Spreading your eggs across many baskets reduces nausea. The longer you’re invested, the more likely it works as expected. And that your investments will always be a distraction in your relationship with money.

Predictably, as our relationship improves, it becomes obvious that "more" does not magically lead to "better".

250 | Permanently Intact

There's an ever-present fear with investing...

What if it all goes to $0?

But once a few important boxes are checked, this isn't really a thing.

Most investment options are more like different apples in the same refrigerated bin than they are different fruits across the produce section.

They all rise and fall together - the biggest ups and downs driven by things we'll never predict.

Up around 20%? So is your neighbor.

Down around 15%? They are too.

Your more is still more, your less is still less - relative wealth always intact.

A lot of marketing dollars are dedicated to making an apple sound like an exotic fruit when it's just a granny smith or pink lady.

And in the impossible event that it all went to $0, you and your neighbor will be more concerned about planting apple seeds than receiving dividends.

249 | Note to Self: Slow the Burn

Dear Richard,

Income's value is infinite until it covers your lifestyle.

And then each extra dollar is a little less valuable.

On the way up, only debt covers a shortfall - a nightmare if left alone.

Extra income that closes the gap is life-changing.

But it's valuable on the way down too.

Because assets burn fast when they're covering every dollar of lifestyle.

But income slows that burn.

Even a modest amount might extinguish it forever.

"We haven't saved enough" is far less deadly than "I can't do this anymore".

Create value more than you hoard it,

Richard

248 | Note to Self: Looking for Signs

Dear Richard,

When you're a little uncomfortable with how much you've made or spent it's a sign.

A sign it's worthwhile to stop making or spending.

Or a sign that you need to bring others into the inner circle.

We're made to be in community with one another.

Ideally, a community that grows in depth over time.

The blind accumulation of "more" doesn't help with depth, nor does more "privacy".

When we long to discover "enough" and to be known by others, that ounce of discomfort is a gift to access both.

Nudging you towards the freedom of transparency,

Richard

247 | Note to Self: Well-Endowed

Dear Richard,

Your head wants to debate, but your heart knows...

An endowment is a scarcity mindset.

Hoarding resources now to help imaginary people later.

And those imaginary people are nonprofit patrons as much as they're you living off 4%.

For a resource dependent on flow, endowing is plaque that leads to triple bypass.

Your head says, "Yes, wealth inequality is a problem."

But that lets you off the hook.

And our world is only the sum of its yous.

Restricting $1,000,000 for a steady stream of $40,000 slows the flow.

And slow flow usurps transformation and hardens the heart.

Graciously planting seeds of change,

Richard

246 | Wise Spending

If your spending isn't growing wiser, I'm not doing my job.

But real enlightenment requires both of us.

Good spending is two things: 1) is the amount we spend responsible? and 2) how do we know we're spending well?

I'll cover #1 every January - a few good data points reveal more than you can imagine.

But #2 is on you.

Only you know what you spent and why.

And a simple way of tracking is the only hope for remembering.

I can help make the tracking easy, but it's still in your court.

Our efforts combined lead to wisdom.

245 | The Master Stroke

Every spending decision has three phases.

The first is every moment before we buy - sometimes minutes, sometimes years.

During this phase, anticipation and hope often add to the magic, while obligation and dread risk hogging the mic.

The second is the precise moment we spend.

The magician loves this phase because it draws all the attention and, to the naked eye, appears to be "financial freedom".

But the third phase - the far side of the decision - is the overlooked master stroke.

Because an infinite loop of first and second phases falsely promises "freedom" that only post-purchase reflection can provide.

The freedom of knowing you'd spend the same way again or honestly acknowledging that you wouldn't.

244 | Two to Tango

When there is something to win - pride, trophy, or money - it attracts competitors.

Comebacks, botched calls, and banners begin to write stories.

But stories can't travel without fans.

And the traveling stories are endless and valuable.

Play games, tell stories, repeat.

The value is that dance, and it only takes two, specifically - those two - to tango.

An extra dancer (or 100!) distorts the dance - "but they led to record revenue" so we press on.

Then one day, a competitor doesn't care to win.

And the 100 remain to fight over the dwindling value.

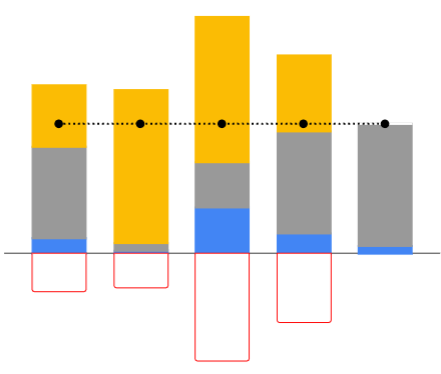

243 | When We Need it Most

The quality of our saving all comes down to access.

Because the same number means wildly different things to different people.

And wildly different things to the same person in a different season.

But the ever-present question with saving is…

Can I tap into what I’ve set aside when I need it most?

Sometimes we pick when we “need it most” and sometimes we’re volun-told.

So here we are, five equally “wealthy” people…

The numbers say they’re the same net worth - the black dots - or the sum of the blue, gray, and yellow less the red.

But which would you pick to be yours?

Does it matter if you love your job?

Or if you hate it?

What if a big spending decision is looming?

Or if one has finally moved behind you?

What if you want to be more generous?

Or if you have a habit of creative generosity?

What if you’re in a season that allows you to save?

Or a season that is forcing you to dip into savings?

We could keep asking questions, but they’ll keep highlighting the fact that saving is more art than science.

242 | More than Counting Beans

Bad accounting is worthless.

Great accounting is priceless.

But how do you know what you have?

If it takes a long time, it’s bad.

If it feels like a burden, it’s bad.

If it is confusing, it’s bad.

If you still don’t know where you stand, it’s bad.

Bad accounting adds stress.

But if it’s quick.

If it’s easy.

If it affirms and clarifies.

If it builds trust.

Then you have great accounting.

Great accounting removes stress.

Bad accounting contradicts the story, great accounting brings it to life.

And if you only know accounting as bean-counting, I’ll let you guess which you’ve seen.

241 | Do We Really Need That Much?

If you’ve accumulated 25 years of spending when you stop working, loads of research says you can increase your spending by inflation every year until you die and you won’t run out of money.

You won’t run out and there’s a great chance you’ll die with more than you had at the start.

We don’t use jargon around here, but if we did, you’d hear this research called the 4% rule.

But it begs the questions…

How many years would be needed if you continued generating some amount of income from something you loved to do?

Or if you were agile enough with spending to delay a big ticket item by a year or two while your investments were down?

Or if you had a good cash cushion and saving spread across account types so you could manage taxes wisely?

Or if you didn’t watch your investments and eliminated the chance of panicking at the wrong time?

It’s less than 25. A whole lot less.

Additional Perspectives

The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement by Michael Kitces

240 | How to “Check Yourself”

“Check yourself before you treat yourself” sounds clever, but how in the “h-e-double-hockey-sticks” do you do it?

It’s only natural to assume that strict guidelines are needed.

But it’s less rules, and more reflection if we’re trying to build a habit that can last a lifetime.

And once we’ve proven we can spend less than we make, that reflection can be simple.

With any spending decision…

Is it a small amount or a big amount?

Is it a one-time occasion or will it repeat?

Is it something we can change easily or are we making a commitment?

If it’s small, one-time, and easily changed then it probably doesn’t need more attention (even if it’s fertile ground for moralizing preferences!).

But if it’s big or likely to repeat or putting us on the hook, then extra reflection is wise…

Will it provide lasting value or only immediate value?

Will it positively impact multiple people or only one?

How is this spending more like an “investment” than an “expense”?

As we ponder these questions, we allow ourselves to begin measuring wealth by more than money.

And we disconnect the decision to spend from the fickle reward of earning.

239 | Homebuying Series: Sprinkle, Don’t Pour

It’s an interesting moment.

Home prices at record highs, and interest rates higher than Millenials imagined possible.

A brutal combo if you’re evaluating a move - particularly away from a pre-COVID interest rate.

But there is an opportunity.

A morale-boosting modification to your current home might be the highest ROI available.

Because $10,000 or $20,000 or even $50,000 is nothing, if it keeps you from doubling your mortgage and doubling the months left till it’s paid off.

Instead of pouring money into a home you might sell, see if sprinkling a little money into it can slowly change your perspective.

And if it does, feel free to sprinkle a little more - your future self will thank you.

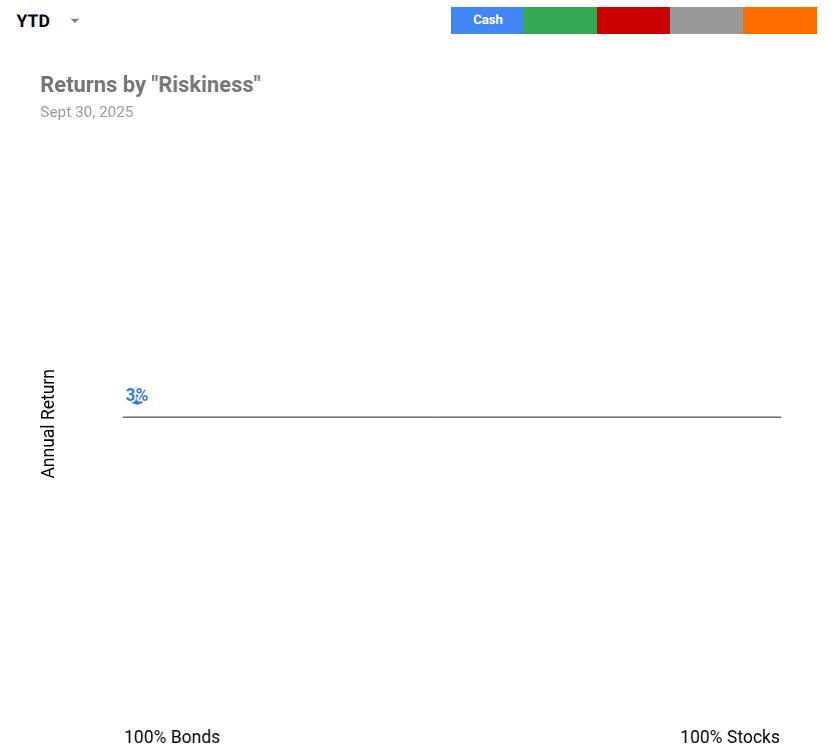

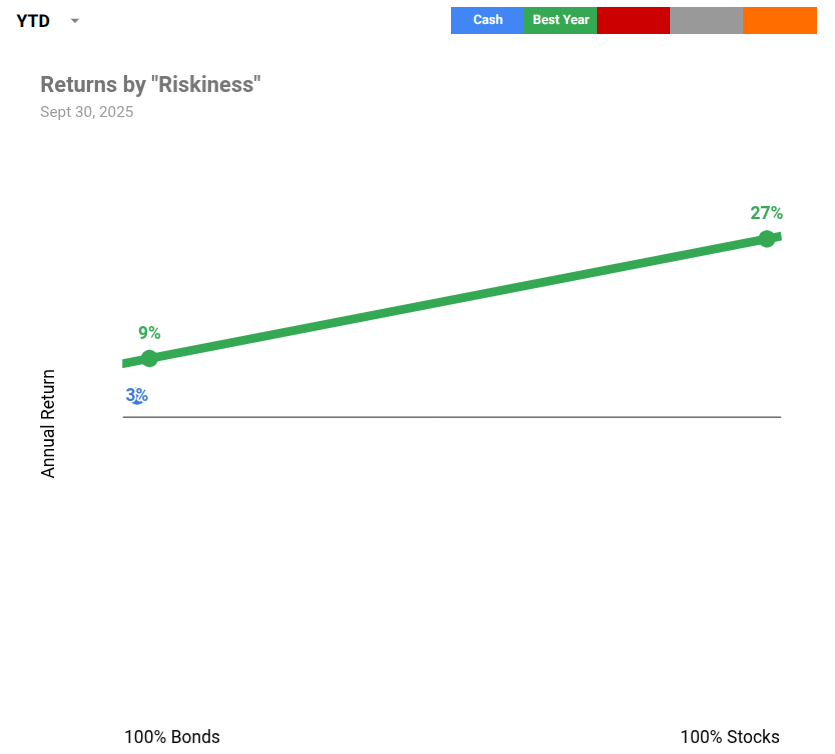

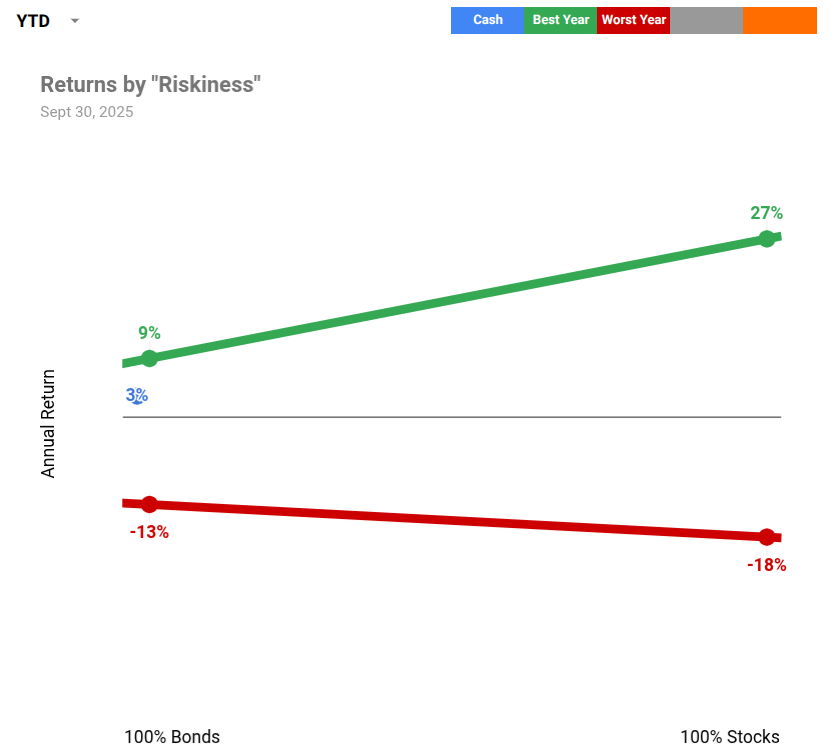

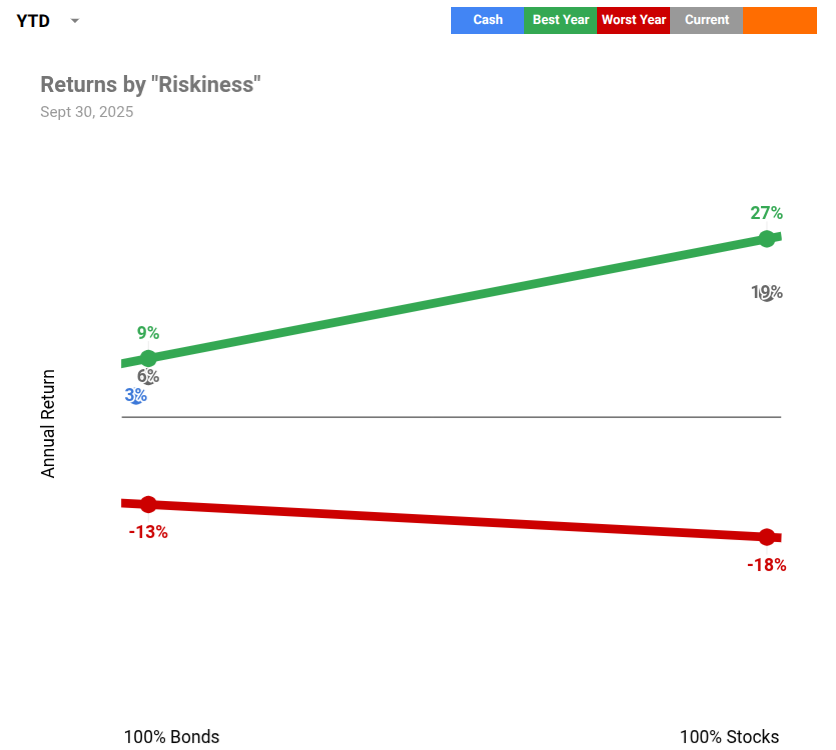

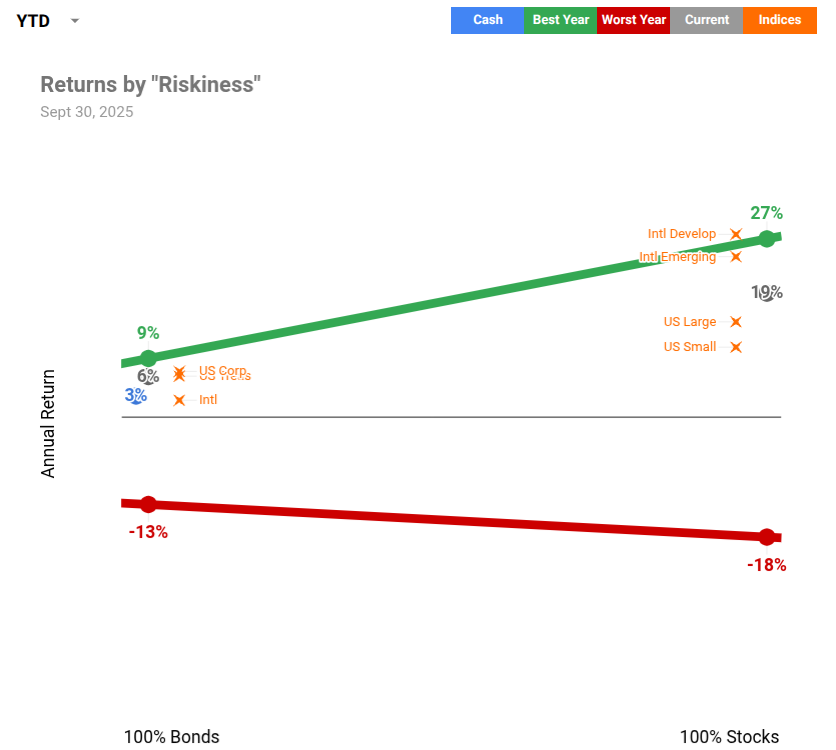

238 | Market Update for Patient Investors: Sept 30, 2025

A market update thru the first nine months of 2025 - if you glaze over when you hear the word “investing”, this update is designed for you.

Interest paid on cash so far this year is the blue dot.

Those are the dollars you see hitting your high-interest savings account each month - fun and novel but not an investment.

Since 2014, the best single year for the average all-stock (relatively more risky) or all-bond (relatively less risky) portfolio is the green line.

A good reminder that owners get the reward for taking the risk.

Since 2014, the worst single year for the average all-stock or all-bond portfolio is the red line.

Owners can be left holding the bag too.

If you want to be “aggressive” with your investments, the wide side of the cone is the place to be.

If you want to be “conservative”, you’d move towards the narrow, left side of the cone.

The gray dots below are for the average all-stock or all-bond portfolio this year.

Since January 1, $100,000 invested in stocks is almost $120,000 and $1,000,000 is close to $1,200,000.

The headlines don’t reflect this reality, but it’s a helpful remainder that you’re usually rewarded for staying invested during the uncertainty - not once everything has “settled down”.

We can’t forget that these dots are a crude summary of the returns for all of the public companies operating around the world.

We could continue drilling down to see each company’s contribution to the whole, but the number of dots would be overwhelming.

The orange x's go one layer deeper to show us the biggest pieces of a typical investment portfolio - the orange x’s on each side roll up to represent the gray dot on their side of the cone.

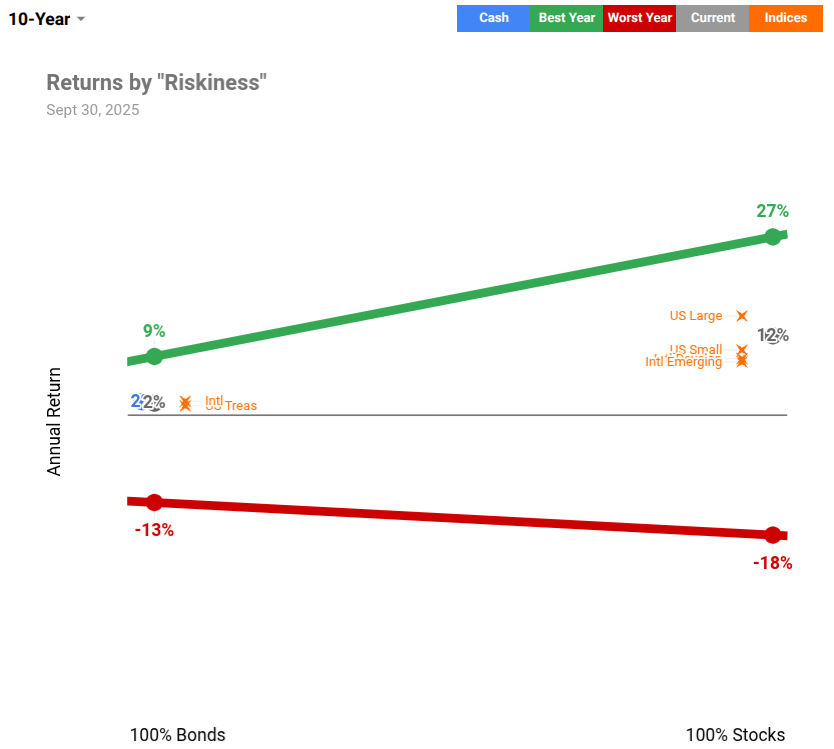

But a good investor doesn’t care about 9 months of returns - that doesn’t move the needle over a lifetime.

When we reflect on the last 10 years, you’d be crazy to complain.

If you’ve stayed invested for the past decade, despite the ups and downs, you made the equivalent of 12% every year for 10 straight years.

In the good times and bad times, patient investing knows that…

Basic understanding enables ignorance.

Someone will always beat you.

Effort ≠ Results.

Owners get the upside (and the other side too).

Spreading your eggs reduces the pain.

The short term can disappoint.

Patience is the only shortcut.

Investments are a distraction in our relationship with money.

237 | Icing the Kicker

A market update is a like icing the kicker before a game-winning field goal.

It’s very noisy. Nerves are high. Things are beyond your immediate control. And it’s best to ignore the consequences.

A coach can say, “Just like you did it in practice.”

“You’ve done this plenty of times before, go and do it again.”

“Breathe, remember your routine, pick your target - then kick it.”

But as soon as you call a timeout, you’re begging doubt, overwhelm, and unforced errors to show up.

And a market update - especially a reactive one - is like icing your own kicker.

In a world where buying and holding runs laps around everything else, you can’t draw attention to information that can only harm.

Remember - the opponent calls the timeout to throw you off your game, not keep you on it.

We don’t like icing our own teammates around here, so we use our timeouts market updates wisely.

Thanks to HS for planting the seed on this reflection!

236 | Love Letters: Why a Kitchen and Living Room Remodel?

I wanted to write this before the project started, but life got in the way, and I’m writing it a little more than a week after we have moved back in.

It is hard to put myself back in the shoes of May 2025, but I still think this is better than not doing it at all.

So here is the love letter to my future self about our decision to remodel our kitchen and living room in the summer of 2025…

Why now?

It feels like we have deferred a kitchen renovation for eight years and it is time to do it to stay ahead of middle school and high school age kids needs

Our income level is at an all-time high and we don’t know if that will continue forever given the general uncertainty of life and career transition plans

Why not move?

It is hard to envision a different neighborhood that we would like to live in within Winston-Salem right now

Our mortgage interest rate is 2.75% and if we were to move and finance the purchase it would be in the 6.5% to 7% range

A move would introduce hard costs associated with the actual move as well as lifestyle creep costs associated with a bigger house in a different location - in some ways, it feels like we are capping our housing cost in ways that will provide significant flexibility for other parts of life that are more important to us

Restarting relationships with new neighbors and dramatically altering relationships with existing neighbors would be a tough pill to swallow

Our top priorities?

To create space to comfortably host and seat 8+ adults in our primary living space

To have an island in the kitchen

To extend the runway on this house and its viability for our family

Why not more?

We quoted a sunroom/living room over the existing deck and a second story on top of that and the entire project would have been between $300,000 and $350,000 - that felt like too much to commit to this house at this point in time, and it also seemed to take the house out of the current neighborhood price range

It seems like we could revisit a real addition of square footage at a future date as our family demands it as the layout of the kitchen would still allow us to easily transition to the deck if needed

We want to believe that our home choice forms our children in ways that are hard to see with a naked eye, and we don’t want our home to be out of place in the West Salem neighborhood

235 | Funky Fees

A fee on managed assets creates some funky dynamics.

At low asset levels, it undermines the advice and makes a client feel weird.

How can the advice be valuable if it’s free?

How can this be a viable business model if I’m not paying anything?

At high asset levels, it still undermines the advice and overcompensates the advisor.

So I guess accumulating “more” is the only objective?

If it’s the same portfolio, why does managing $1,000,000 cost more than $100,000?

If it feels funky, it probably means there is a better way.

234 | Taxophobia

I hate taxes.

And it’s not because I have to pay them.

It’s because of the way they keep us from turning real financial wealth into other forms of wealth.

Fear of paying taxes loves to keep us from a better version of our life - “taxophobia” if you will.

You know the cycle…

Make money. Yay!

Realize later on that you have to pay taxes. Noooooo!

This cycle is disappointing, but not necessarily life altering.

It’s when we’ve made money, but still have control over when we will (or won’t!) pay the taxes that’s the real monster under the bed.

The sale of capital gains that would trigger a tax bill.

The withdrawal from a retirement account that would be complemented by taxes.

The cancelling of life insurance policies that would add to what we owe in April.

And so wealth tends to accumulate forever without being used for anything more than its “security” because we’re afraid to pay the tax.

Inevitably, you will pick a side - taxes as feature or taxes as a flaw of life on earth.

If you’re courageous enough to see them as a feature, it’s easier to experience the freedom your wealth provides.

Picking the other side often makes you stingy, skeptical, and grumpy.

233 | X-Rays

We tend to think of tracking spending as counting calories.

And since calorie counting is usually a tool for weight loss, tracking becomes nothing more than a discouraging way to limit your spending.

One that amplifies guilt or shame, restricts freedom, and feels like a repetitive slap on the wrist.

But this robs it of its purpose and power.

Tracking spending isn’t calorie counting, but an x-ray machine.

X-rays carry no judgment.

They give no snarky self-talk.

They provide no critique or restriction.

They can even come back negative because nothing is broken.

No combo of rest, ice, compression, and elevation can touch the peace of mind and clarity that comes from a quality x-ray.

A quick peek under the surface is the most painless route to full activity levels.