The Good Relationship

A blog that knows money is never just the numbers

Click a category to dive deep:

Relationship with Money

Sustainable Income

Accessible Saving

Why We Love Our One Pager

Why We Don’t Manage Assets

Content Spending

Patient

Investing

Why We Don’t Predict

Why We Prefer a Flat Cost

250 | Permanently Intact

There's an ever-present fear with investing...

What if it all goes to $0?

But once a few important boxes are checked, this isn't really a thing.

Most investment options are more like different apples in the same refrigerated bin than they are different fruits across the produce section.

They all rise and fall together - the biggest ups and downs driven by things we'll never predict.

Up around 20%? So is your neighbor.

Down around 15%? They are too.

Your more is still more, your less is still less - relative wealth always intact.

A lot of marketing dollars are dedicated to making an apple sound like an exotic fruit when it's just a granny smith or pink lady.

And in the impossible event that it all went to $0, you and your neighbor will be more concerned about planting apple seeds than receiving dividends.

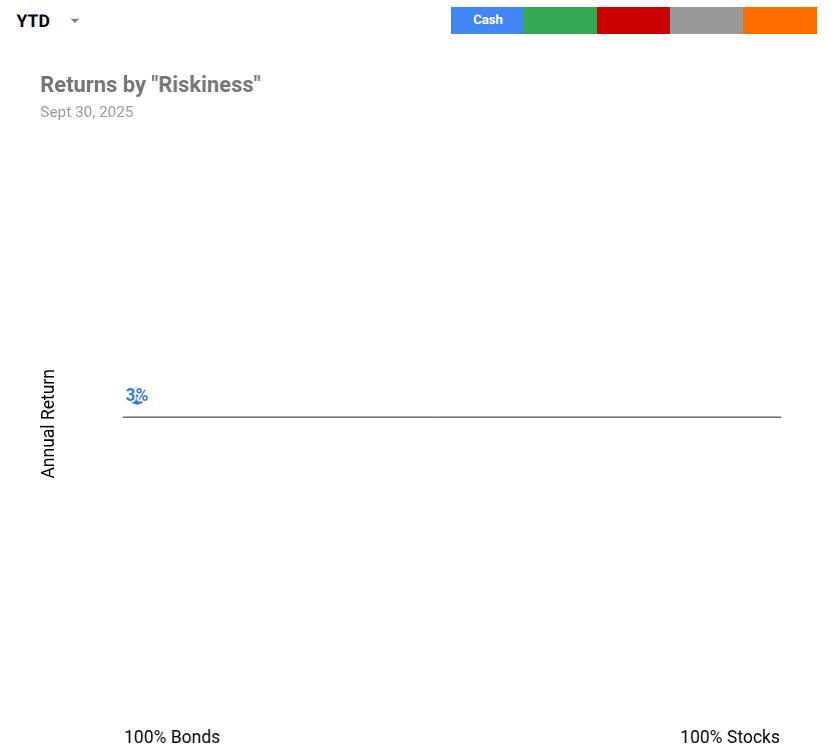

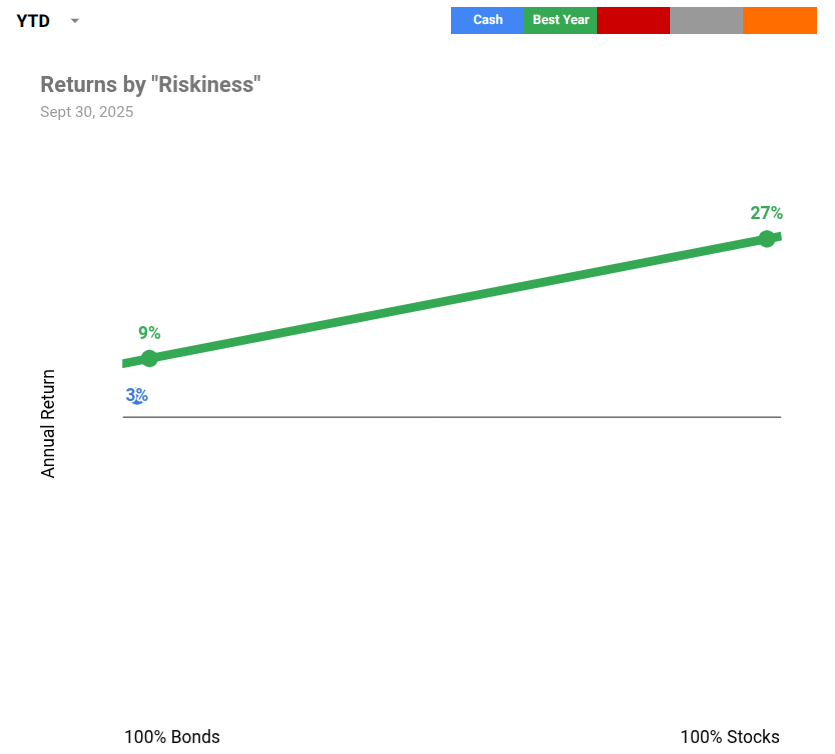

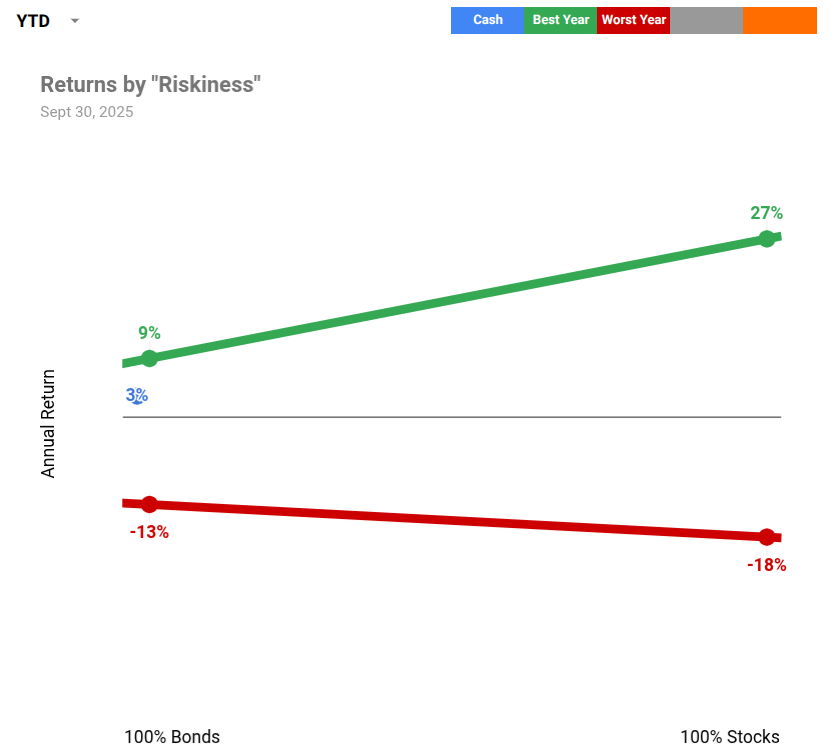

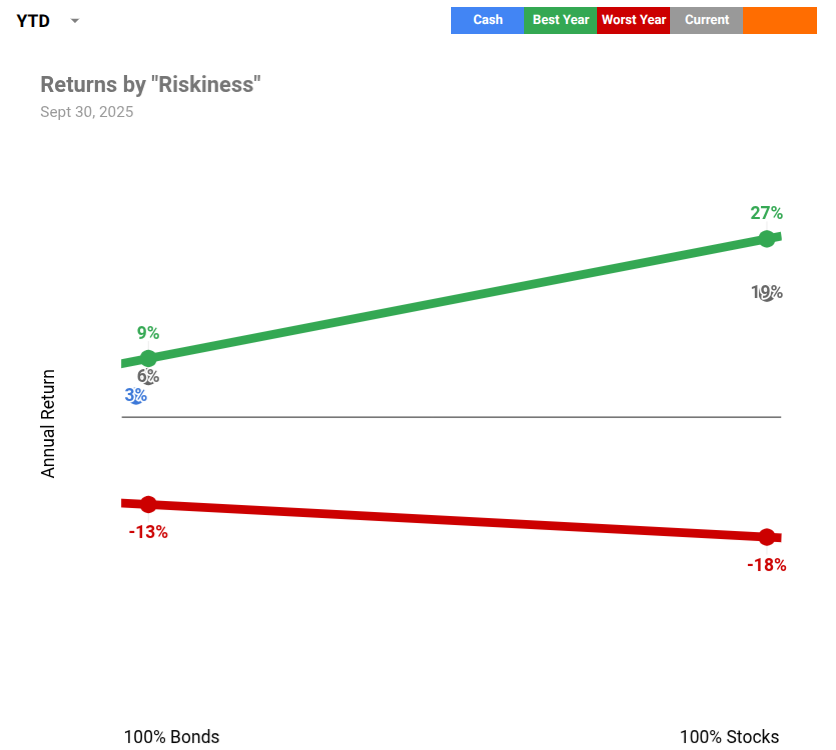

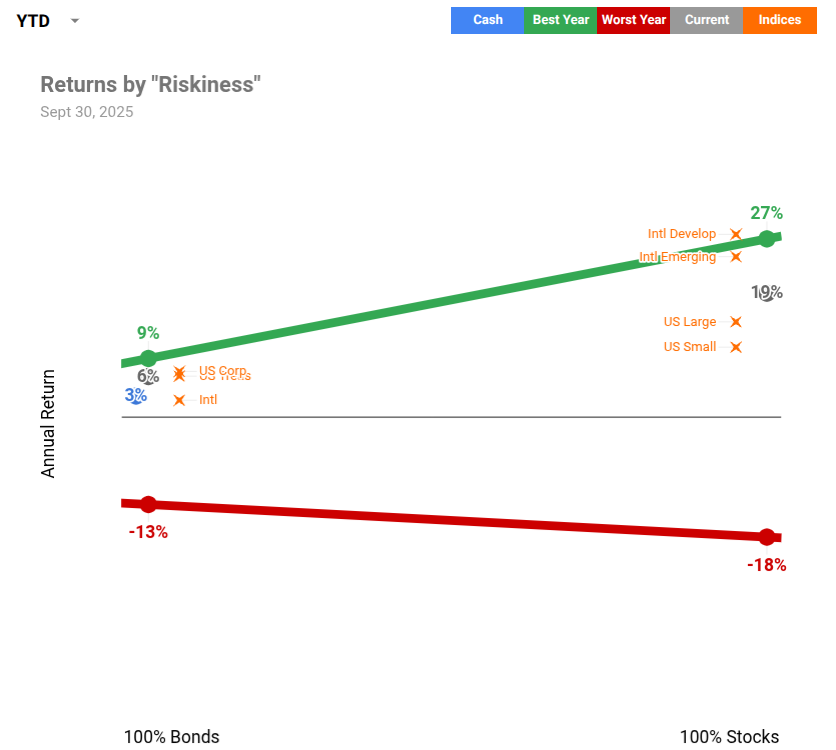

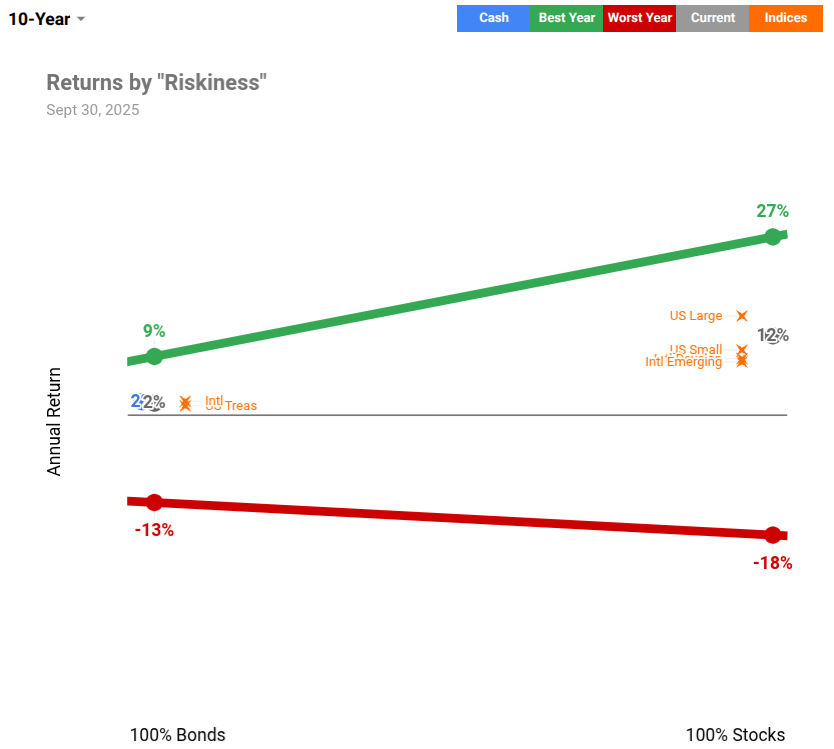

238 | Market Update for Patient Investors: Sept 30, 2025

A market update thru the first nine months of 2025 - if you glaze over when you hear the word “investing”, this update is designed for you.

Interest paid on cash so far this year is the blue dot.

Those are the dollars you see hitting your high-interest savings account each month - fun and novel but not an investment.

Since 2014, the best single year for the average all-stock (relatively more risky) or all-bond (relatively less risky) portfolio is the green line.

A good reminder that owners get the reward for taking the risk.

Since 2014, the worst single year for the average all-stock or all-bond portfolio is the red line.

Owners can be left holding the bag too.

If you want to be “aggressive” with your investments, the wide side of the cone is the place to be.

If you want to be “conservative”, you’d move towards the narrow, left side of the cone.

The gray dots below are for the average all-stock or all-bond portfolio this year.

Since January 1, $100,000 invested in stocks is almost $120,000 and $1,000,000 is close to $1,200,000.

The headlines don’t reflect this reality, but it’s a helpful remainder that you’re usually rewarded for staying invested during the uncertainty - not once everything has “settled down”.

We can’t forget that these dots are a crude summary of the returns for all of the public companies operating around the world.

We could continue drilling down to see each company’s contribution to the whole, but the number of dots would be overwhelming.

The orange x's go one layer deeper to show us the biggest pieces of a typical investment portfolio - the orange x’s on each side roll up to represent the gray dot on their side of the cone.

But a good investor doesn’t care about 9 months of returns - that doesn’t move the needle over a lifetime.

When we reflect on the last 10 years, you’d be crazy to complain.

If you’ve stayed invested for the past decade, despite the ups and downs, you made the equivalent of 12% every year for 10 straight years.

In the good times and bad times, patient investing knows that…

Basic understanding enables ignorance.

Someone will always beat you.

Effort ≠ Results.

Owners get the upside (and the other side too).

Spreading your eggs reduces the pain.

The short term can disappoint.

Patience is the only shortcut.

Investments are a distraction in our relationship with money.

237 | Icing the Kicker

A market update is a like icing the kicker before a game-winning field goal.

It’s very noisy. Nerves are high. Things are beyond your immediate control. And it’s best to ignore the consequences.

A coach can say, “Just like you did it in practice.”

“You’ve done this plenty of times before, go and do it again.”

“Breathe, remember your routine, pick your target - then kick it.”

But as soon as you call a timeout, you’re begging doubt, overwhelm, and unforced errors to show up.

And a market update - especially a reactive one - is like icing your own kicker.

In a world where buying and holding runs laps around everything else, you can’t draw attention to information that can only harm.

Remember - the opponent calls the timeout to throw you off your game, not keep you on it.

We don’t like icing our own teammates around here, so we use our timeouts market updates wisely.

Thanks to HS for planting the seed on this reflection!

230 | Give Me Snail Mail

Technology makes things faster, but not always better.

Dividend checks used to show up in the mail every month or quarter or year.

If the market was up, there was a check.

If the market was down, there was still a good chance of a check.

Real income that repeats year after year after year…even when our investments are down in value.

That sounds sort of nice, particularly in a world of people who spend income more freely than they spend their savings.

Dividends haven’t gone anywhere, but their automatic reinvestment has made it feel like they’re being returned to sender or forwarded to the wrong address.

Instead of a paper check reminding us that we own real businesses making real money, we watch account balances move in apps like modern-day Monopoly money.

And Monopoly money is hard to spend in the real world.

Sometimes a little friction enables a lot of freedom.

229 | Market Update for Patient Investors: June 30, 2025

A market update for normal people thru the first six months of 2025.

Interest paid on cash so far this year is the blue dot. Cash is never to be confused as an investment - "no risk = no return" even if you have a good interest rate.

Since 2014, the best single year for the average all-stock (relatively more risky) or all-bond (relatively less risky) portfolio is the green line. An ongoing reminder that stockholders get the biggest rewards.

Since 2014, the worst single year for the average all-stock or all-bond portfolio is the red line. Stockholders have the most heartache too.

Folks with a paycheck often aim for the wide side of the cone, those without one tend to aim for the middle.

The gray dots below are for the average all-stock or all-bond portfolio this year. So far an above average year, despite the shock of tariffs and the doom of headlines.

Since January 1, $100k invested in stocks is now ~$110k and $1m is ~$1.1m.

Here is where it's helpful to remember our investments aren’t a black box. When we invest, we own teeny slivers of real companies operating in the same uncertain world we experience each day.

The gray dots are a blend of all public companies from all over the world - the orange x's go one layer deeper to show us smaller pieces of the gray dots.

But remember whether these six months had been good or bad, it’s not about the days or months or years when we invest, it’s about the decades. And it's hard to be disappointed over a decade. The gray and orange are annualized returns for the past 10 years - a fancy way to say it’s like you got 10% every year for 10 straight years.

In the good times and bad times, patient investing knows that…

- Basic understanding enables ignorance.

- Someone will always beat you.

- Effort ≠ Results.

- Owners get the upside (and the other side too).

- Spreading your eggs reduces the pain.

- The short term can disappoint.

- Patience is the only shortcut.

- Investments are a distraction in our relationship with money.

224 | Pick Your Poison

There are really only two ways to invest - hold them all or pick a few good ones.

A lot of research here shows it's pretty hard to distinguish which approach is better.

Holding them all guarantees you don't miss the best ones, but it means you'll hold the worst ones too.

This way is almost always a smoother ride.

It's also less "expensive", which is a special way to say no one's analyzing much of anything.

Picking a few good ones can be extraordinary...as long as you pick the right ones.

If the few you pick are wrong, you'll be sad. And whether you pick well or not, it will be a wild ride.

This way is more "expensive" - sometimes in dollars, always in minutes - but intellectual or moral "consideration" is valuable to many folks.

Both approaches can, and do, work. Both have seasons of disappointment too.

Instead of arguing about the approach, it's best to pick the one that resonates most and then move on.

If it seems I’ve oversimplified it, here's the fancy version...

"The data on wealth creation suggest two strategies for portfolio construction. One is to recognize that an investor can capture the skewness, or asymmetry of a distribution, in long-term total shareholder returns by holding a diversified portfolio. Index funds are an effective way to implement this approach. While an index will include stocks with poor returns, it will also have the handful of companies that generate most of the aggregate value. The other strategy is to build a relatively concentrated portfolio that seeks to include the companies that have the potential to generate high returns and avoid those that do not."

222 | More Thoughts on Investment Properties

Investment properties work well for four types of people.

- Those who pay minimal (maybe $0) closing costs.

- Those who are handy enough to fix things themselves.

- Those who have lots of discretionary time.

- Those who want it for non-financial reasons.

If you aren't one of those four types, it's gonna be a frustrating road.

218 | Financial Obituaries

Your investment experience will not define your financial life.

That is, as long as you've spread your eggs across a couple baskets, aren't using short-term debt to juice your returns, and aren't buying and selling based on daily movement.

Everyone's investment experience is too similar - all rise, all fall - for it to be any other way.

And if it’s not unique to you, how could it possibly get a line in your financial life’s obituary?

Even the worst-case scenario of everything going to $0 wouldn’t be that defining because financial wealth is relative.

And everyone else would be strapped in beside you for the ride down - leaving your relative wealth secure.

Our financial obituaries might say...

- He grew to love his work and changed the lives of clients and co-workers.

- She saw the value of things, not just the price.

- He knew money spent on relationships was an investment, not an expense.

- She never tried to predict the future, but was always calm when it arrived.

- He appreciated that "enough" was a lifestyle more than a number.

But they'll never say...

- She kept cash on the sidelines and then capitalized on every recession.

- He beat the S&P 500 in eleven different years over his lifetime.

- Their life would have been better if they'd made 2% more per year.

215 | No Action Required

It can be painful to realize we're not in control.

And our investments are particularly adept at revealing this reality.

If you haven't noticed this time, kudos to you, you won't find a more accessible or powerful investing skill than intentional (even unintentional!) ignorance.

Feel free to stop reading here and keep living life.

If you have noticed, then it's served as a helpful reminder of why we do what we do.

Sometimes it seems overkill to be so careful with cash.

Or to start the year by understanding our entire financial life with a few colors and bars.

Or to talk about all the other parts of our financial life that are more in our control and add all the color to life.

But then uncertainty begins to connect the dots for us.

We do these things, because they prepare us for the seasons where it's better to look away for a moment than to stare.

Better to be still than make a regrettable move.

Better to see it as a workout making us stronger for the next one than a hole leaking water out of our bucket.

Additional Resources

For those who like motivational speeches, read more here.

For those who like history, read more here.

For those who like numbers, read more here.

214 | "The Market" isn't Hard to Predict

"The market" is nothing more than a live streaming estimate of the financial emotions of everyone on Earth.

Me. You. Your neighbor. That stranger in traffic. That person on TV. That person who makes you cringe. That other person who cancelled your vote in the last election. And the other 4 or 5 billion adults walking the planet.

Each of us, tuned in (or not!) to the news.

Each of us, tuned in (or not!) to our emotions.

And then…

Each of us, making an investment decision (or not!) based on one or both of those things.

It’s not the news or even the emotions that move “the market”.

But the collective “buying-and-selling” decisions of everyone in the world based on their news and their emotions…and their businesses.

If those who are encouraged by the future ("buyers") outnumber those who are discouraged ("sellers") or apathetic ("holders"), “the market” goes 👆🏻.

If the folks who are discouraged by the future outnumber the encouraged or apathetic, “the market” goes 👇🏻.

"The market" isn't hard to predict - it's the people that are tricky.

211 | Don't Get Distracted

Investing is a lot like running.

We run to keep our fitness up and often measure progress by tracking our time.

Some years we trim 10 or 15 seconds off our personal record and don't even notice.

Some years we roll an ankle or get too busy and some seconds are added back to our time.

Sometimes we see someone else running faster or we hear about a new technique or we hire a coach that introduces a new regimen and our times bounce up and down.

If we're not careful, the stopwatch begins to distract us from our actual fitness.

Our 6:10 mile from two months ago doesn't make today's 6:16 mile or tomorrow's 6:20 mile a signal that our fitness is spiraling.

Don't get distracted by the times. Just keep running.

210 | Cashing in on Excitement

There are only three ways to make money investing.

- Lend money to someone who pays you while they borrow* (interest)

- Own something that makes money and pays the profits to you (dividends)

- Own something while the excitement around it grows (capital gains)

The last way offers the most upside, but it's impossible to predict.

Sometimes profits trigger excitement around a company.

That excitement rewards the founders.

Sometimes excitement surges, but a company never turns a profit and excitement fades.

That excitement rewards the lucky (or the reckless!).

Sometimes a company is exciting and profitable.

That excitement rewards the patient.

The only way to cash-in on excitement is to own the company...

While the excitement builds.

If you wait for excitement to grow, you've missed out.

If you're not a founder, be careful.

*Ideally, they return whatever they borrowed at the end.

207 | That Person Doesn’t Exist

"If only I'd bought ________ in 20__*, then I could kickback today."

But the person that can do those two things doesn't exist.

"Buying and riding" isn't a thing like "kicking back with your feet up".

If you stay on the ride, you're dancing with ruin on the daily.

And if you get off the ride, you'll second guess all the upside you left on the table until the end of time.

Neither sounds much like "kicking back".

At some point, you have to decide if you're investing to live life or living life to invest.

*Today's mad lib would be Bitcoin in 2011, but there are as many examples in the past as there will be in the future.

202 | Dirty T-Shirts

We can talk about past performance.

We can talk about future projections.

We can talk about the nitty gritty details of our investments.

But none of it will impact how our investments actually perform.

It's a little like wearing the same t-shirt for every game of your team's playoff run to help them win.

It makes us feel like we're in control, but we all know we're not...right?

We don't jump past investment talk because we're afraid or unprepared to do it.

We move past it because anything else might convince us to keep wearing that dirty t-shirt.

201 | Riding the Wave

“I'm hesitant to invest because I don't want it to go down.”

But....

“I don't want to miss out on the next wave.”

Well yeah...me neither.

But that's the water we'll be swimming in from now until the end of time.

Investments that will go down.

And waves that will keep coming.

You don't get one without the other, and nobody knows when either will happen.

That's the main reason that we're careful when we're getting started.

Because if we get spooked on our first drop, then it's going to be harder to catch the next wave.

And riding the wave is a lot more effective than swimming back to shore.

181 | The Primary Question of Each Recession

The stock market is a lot like humans - it’s not big on uncertainty.

When the future feels less certain, the stock market and its underlying businesses tend to decrease in value.

When the future feels more certain, they tend to increase in value.

Of course it's this way because “the stock market” is only the sum of humans’ perceived uncertainty about the well-being of the world’s businesses.

Most of the time, one person’s uncertainty is offset by another person’s certainty, so we get negligible changes in the value of the entire market.

But one or twice a decade, there are single questions that make almost everyone feel uncertain…

2022 - Were we too optimistic about our rebound from COVID?

2020 – How many people are going to die from COVID?

2008 – How many people made a bet on or were debtors to a bad mortgage?

2002 – How many companies do not have a viable business model?

Nearly 100% of the market decline in each of these seasons could be tied to our collective inability to answer these questions.

And the subsequent market rebounds happened as the answers to these questions became less squishy.

Not by coincidence, none of these questions had a thing to do with the next president, a change to tax code, or a Federal Reserve interest rate adjustment.

The next recession will likely be the next time we have an unanswerable question, it’s just hard to know the question before it’s asked.

180 | Perpetually Uncommitted

The holy grail in investing is a level of commitment that can see beyond benchmarks, novel products, and market forecasts.

A basic understanding and set of beliefs that underpin the way you've decided to invest that slowly reduces your desire to evaluate or even acknowledge alternatives.

Not like an ostrich with its head in the sand, but more like a spouse that stops evaluating candidates for marriage once they've said, "I do."

There's a freedom that comes from commitment.

And an anxious prison that comes from the endless search for something else.

Seeing a headline about the highest performing stock of the year - an invitation to de-commit.

Catching a bad market cycle in your first year with an advisor - an invitation to de-commit.

Presuming that someone's elevated lifestyle choices are a direct result of their investment savviness - an invitation to de-commit.

Seeing your account lag a benchmark, a friend, or a faulty expectation - an invitation to de-commit.

Just like a relationship, once we commit, there is peace of mind, freedom from second-guessing, grace for mishaps and disappointment, and compounding that begins to surpass all expectations.

That sounds like a good outcome.

171 | Patient Investing

Investing with some clue about what you're doing and a genuine belief that it will work.

Knowing there are only two guarantees:

1. Someone will always have better returns than you.

2. The way you behave, especially when it's uncomfortable, will determine your lifetime returns.

Being an owner offers the most potential reward.

Spreading your eggs across many baskets makes the uncomfortable times less painful.

The longer you're invested, the better chance that it works as expected.

And a little more patience than the next person is the only shortcut.

And…

Investments will almost always be a distraction in your relationship with money.

168 | A Percent of What?

The entire industry is built on rate of return.

Your portfolio returned 21% last year.

This investment has returned 10% per year for the past 5 years.

We project that you can earn 8% per year over the next 20 years.

But percentages aren't that helpful.

When we're dealing with small numbers, the percent return is useless.

A 20% return on $10,000 means that you have $12,000 and that isn't going to change any lives.

When we're dealing with big numbers, the percent return is equally misleading.

A 20% return on $1,000,000 could be a couple of extra years of spending or a college education or a down payment on a home - significant increases in financial freedom that would still exist at 15% or 17% or 22% or 26%.

All the percent sign does is beg us to compare ourselves to others, which isn't very helpful at any number size.

Or forget what we were aiming for when we decided to invest.

166 | So Little Control

We can do everything right when it comes to investing - control costs, manage taxes, properly diversify, get the right blend of stocks and bonds, have a long horizon, and behave as well as the best investor.

But the actual timing of returns is still so far out of our control that it's scary.

Most everyone would be comfortable, probably even recommend, using the past 30 years of returns to project the next 10 years of returns.

Anything more elaborate than that quickly becomes a waste of time and energy.

But on our journey to life changing returns, the timing of those returns can change the trajectory of our life.

In 1988, if you had $250k invested and used the return for the previous 30 years to predict your balance by 1998, you'd expect to have $428k, but would have ended up with $1.1m. Check the math here.

Saving for an addition to your home? How about an addition and a second home and a career change and a college education or two?

In 1999, you'd have expected $629k by 2009, but would have ended with a meager $190k.

In 2011, you'd have expected $543k by 2021, but would have ended with a whopping $947k.

And remember, this is the experience when you're investing the right way.

It seems like we have two choices.

We can try to saddle up for the bull ride of investing and tether our financial well-being to every jolting buck.

Or we can acknowledge that while powerful, our investment returns tend to be a distraction from where our life - generating income and spending and saving it - is actually lived.